If you are losing your sleep at 5% or 10% of stock market correction, then you do not have the stomach for volatility and have low risk appetite.

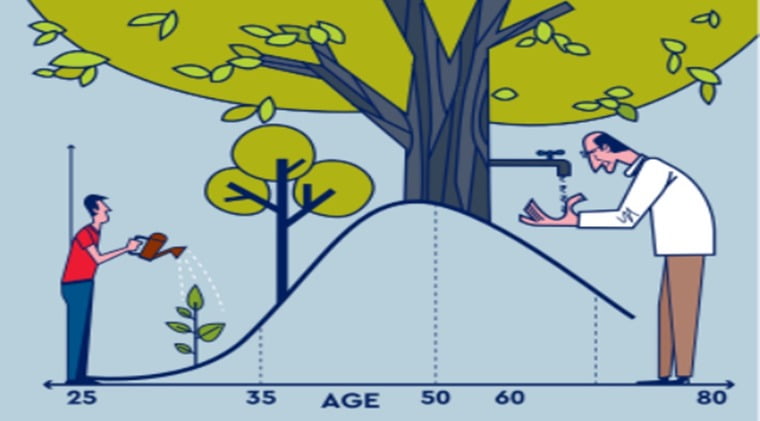

Financial planning wisdom says our financial life is divided into broadly three phases: accumulation, consolidation and distribution. Accumulation phase starts when you start earning, at, say, 25 years age. However, in the real sense, it starts when you start saving and investing, for your future. For the consolidation phase, there is no hard and fast definition, but broadly age 50 to 60 is taken as the consolidation phase. This is the time when you take a look at your finances, review it, and prepare for your retired life. In this context, retired life means when you don’t have any active income. Distribution phase is your retired life, when you live off what you have earned and worked for throughout your life.

Three phases of financial life

What is the relevance of dividing your financial life into three phases? In the accumulation phase, you have a long time horizon ahead, your risk appetite for investments is higher and don’t have to care unduly about the risk profile of the investments in your portfolio. In the consolidation phase, along with advancing age and approaching retirement, you have to take care. You have to review the risk profile of your investments and consolidate, which is why it is called consolidation phase. The distribution phase is called so because you are distributing to yourself, what you earned and accumulated over your life.

This discussion is about the consolidation phase. Conventional wisdom says your exposure to risky investments such as equity should be relatively lower and exposure to relatively stable assets like fixed income should be higher. This is in keeping with your risk appetite, with retirement approaching. The thumb rule says 100 minus your age should be in risky assets like equity. As an example, if your age is 60, then 40% allocation in your portfolio should be in equity and 60% to fixed income or stable (i.e. less volatile) assets. Conventional wisdom is correct, as it has evolved through practice, over time. However, keep these aspects also in mind:

Allocation to debt and equity

Allocation to debt and equity is a function of your risk profile and requirements. Each individual is unique, and risk appetite, while it comes down with age, is different for each individual. At age 60, if 40% exposure to equity or other volatile assets seems high in times of market fluctuation, keep it on the lower side. On the other hand, if you have a proper realisation of the extent of potential volatility and you are okay with it, you may keep it on the higher side as well. A simple gauge here, of your risk appetite, is at what extent of return down-tick you would lose your sleep and wish you had not made that investment. If your threshold is 5% or 10% return down-tick, then your risk appetite is low. If it is, say, 20% or 30% of market correction, then you have the stomach for volatility. In terms of volatile assets, not just equity, but gold also can be volatile to an extent.

The other aspect is, when the investments in your portfolio are old enough and have earned for quite a period of time, a cushion builds up. For a perspective, if you invested at Nifty level of say 10,000 and currently it is at say 17,300, then your portfolio also has grown. In fixed income investments, there is accrual, which grows your cushion. The point here is, when we count return drawdown, we are not consciously aware, but we are counting from the peak. From the high point of Nifty at 18,600 it has corrected 7%, but depending on your investment level, it has growth significantly. As in this example, from 10,000 to 17,300, it has grown that much.

Post retirement, along with advancing age, you can do a gradual re-alignment of your portfolio allocation, as per your needs and requirements.

Source: https://www.financialexpress.com/money/your-money-how-much-risk-is-too-much-risk-for-you/2486193/